Stress Testing in Financial Modeling

Financial modelling is at the center of sound business decision making. To what extent your model is useful depends on how good it is, and to a greater extent, how testable the assumptions are, whether you are considering a possible acquisition, developing a business case to support internal investment or preparing a round of fundraising. Stress testing and sensitivity analysis are two of the most important but least developed in this space. These methods make a given financial model dynamic and capable of modeling a business performance in the case of a change in conditions.

Stress testing and sensitivity analysis is not a mere theoretical exercise to professionals who are taking financial modeling courses. They are practical models which assist the analysts to answer one of the greatest questions that a decision-maker will ask ever: What happens if we are wrong? This paper discusses the ways these techniques operate, why they are important, how they are used in practice and what has been learned by practitioners in the process. This guide is intended to provide a systematic and practical knowledge of both concepts to both a junior analyst, who is developing his or her first three-statement model, and a mid-level professional, who wants to enrich his or her toolkit.

It is notable that stress and sensitivity tests cannot be used interchangeably although they are closely related. Sensitivity analysis looks at the impact of a single variable, e.g., revenue growth or cost of goods sold on the outcome of a model, when it is varied independently. Stress testing, on the other hand, is the process of running a combination of negative assumptions at the same time, to check how the model performs in the worst or near-worst-case conditions. They go hand in hand and are the keys to the strong financial analysis.

Understanding the Difference: Sensitivity vs Stress Testing

Of the two methods, sensitivity analysis is possibly the more well-known. In simplest form it is the process of varying one input variable e.g. the gross margin percentage and then tracking the impact of the variation on a major output such as net income or free cash flow. This type of one-variable sensitivity analysis is occasionally referred to as a one-way sensitivity analysis. A more sophisticated form is a so-called two-way sensitivity, or analysis of the interaction of two variables. An example would be a grid of revenue growth rates, and operating cost assumptions, how net income and debt coverage ratios vary?

Stress testing is further extended by building up defined scenarios, with three commonly used scenarios being a base case, a downside case and a severe stress case: in a severe stress case, several variables change in the wrong direction simultaneously. Stress testing does not involve pushing a single lever at a time, but instead pulls multiple levers simultaneously to recreate the state of the economy such as a recession, or a supply chain disruption, or the abrupt death of a key client. Stress testing was introduced as a regulatory requirement of the banking industry as a result of the 2008 world financial crisis but since then the practice has permeated corporate finance, private equity and start up funding.

To analysts who are taking a course in financial modeling, using a scenario based approach, the difference is evident in practice. Scenario based modeling requires you to specify what kind of world you are modeling – what events and conditions occur – before you even see the numbers. This format promotes better reasoning and more justifiable assumptions and that is why it has been adopted as a standard in the industry in most serious financial modelling situations.

Table 1: Sensitivity Analysis vs. Stress Testing — Key Differences

| Dimension | Sensitivity Analysis | Stress Testing |

| Variables changed | One or two at a time | Multiple simultaneously |

| Purpose | Understand output sensitivity | Strain-resilience of test model. |

| Complexity | Low to moderate | Moderate to high |

| Common use | Model building, presentations | Risk analysis, money raising, borrowing. |

| Typical outputs | Data tables, tornado charts. | Scenario waterfall, coverage ratios. |

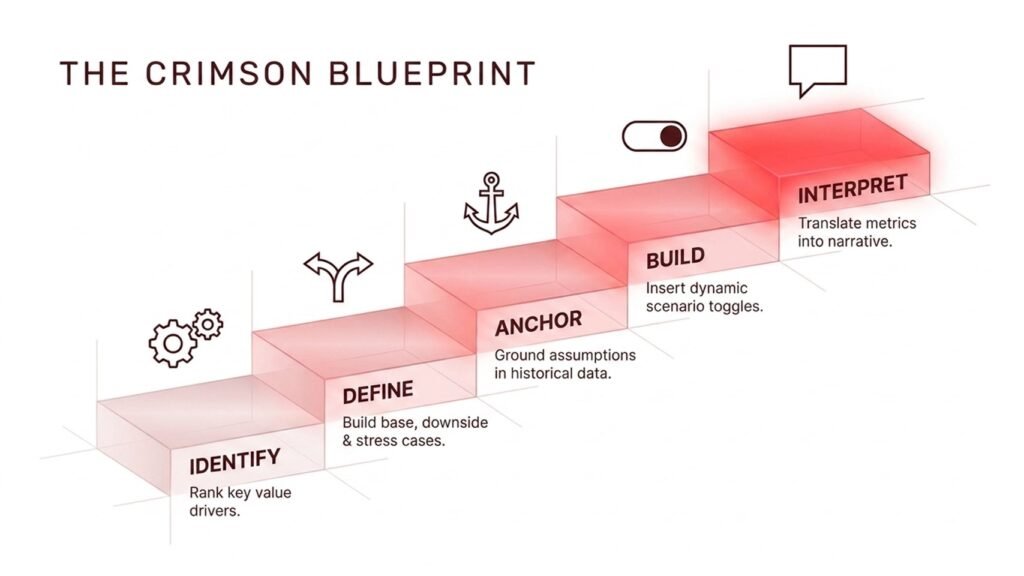

Building the Foundation: Five Key Steps to Effective Stress Testing

Successful stress testing is not an accident. This needs to be done in a systematic way that begins long before keying in numbers in a spreadsheet. The next five steps are the best practices of stress testing that an analyst should apply when he/she is taking financial modeling courses or in real life situation when he/she is working professionally.

The first step will be to determine the crucial business value drivers. To be able to stress a model, you must be aware of what assumptions are important. Volume and average selling price are likely to be the drivers in a retail business. The monthly recurring revenue growth and churn in a SaaS company may be the case. With your sensitivity analysis, you can make a tornado chart, which is a horizontal bar chart that orders variables by their contribution to a target output, to find out which of these drivers you should focus on the most.

The second step is to specify your scenarios. You ought to have at least a base case, a downside case and a stress case. The base case is an estimation of the best future you have under the existing information. The worst case scenario could indicate a relatively small decline – perhaps the revenue is 10-15 percent less than forecasted. The stress case is the real test: what would happen in case the revenue is reduced by 30 percent, the margins are decreased, and the working capital requirements are raised simultaneously? The third step is to ground your assumptions on the real-world facts. Stress situations are not to be random. Resort to history: To what extent are industry revenues decreasing during the 2020 COVID-19 lockdowns? What was the experience in the credit spreads in the 2008 crisis? Basing your scenarios on facts makes them more acceptable to both lenders and investors as well as to the management.

The fourth step is to assemble the mechanics into your model properly. It consists of having a distinctly marked scenario switch, typically a dropdown or a numbered input that requires the switching of case assumptions, instead of in-lining stressed values. This makes your model auditable and enables you to present a large number of cases with ease without having to override them manually. The fifth step is to communicate and interpret the results. It is not just half of the story of the numbers. What is their meaning in terms of liquidity? Is the company violating a debt covenant as a part of the stress case? What is the number of months of runway? This number-to-story translation is what makes the difference between good analysts and great ones- and it is another skill that will be acquired with practice in systematic financial modeling courses.

Table 2: Stress Testing Process Flow

| Step | Action | Output |

| 1 | Determine important value drivers through sensitivity analysis. | Ranks list of drivers / tornado chart. |

| 2 | Identify structure of scenarios (base, downside, stress) | Scenario framework document |

| 3 | Reference to historical or market data. | Assumption log including the sources. |

| 4 | Import the financial model with build scenario switch. | Dynamic, auditable model |

| 5 | Interpret findings and put into story. | Memo or report on stress test. |

Real-World Application: Lessons from Actual Cases

Concepts are practicalized by theory, but concrete examples are case examples. Suppose an example of a medium-sized airline in Europe in the early months of the COVID-19 pandemic in 2020. The finance team at the airline had developed a typical three-year financial model where the base case was that of 5 percent growth in revenues and that of stable fuel costs. The team scrambled to stress test the model real-time when travel restrictions struck. Their base case of the first downside presupposed the decrease in revenues by 30 percent – however, the decrease in revenues was about 75 percent during the most severe periods of lockdown. The instruction was to avoid the failure of the model, rather than to the fact that the stress cases had not been attracted out of a sufficiently adverse historical precedent. They could have thought more drastic things, had the team mentioned the post-9/11 or SARS-era downturns in aviation.

The other educational case is in the startup world where stress testing overlaps with the startup valuation and fundraising masterclass environment. One of the e-commerce startups in Southeast Asia was about to undertake a Series B raise, and had constructed an investor-facing financial model forecasting 3x revenue growth in 3 years. As part of due diligence, the team of the lead investor conducted a stress case whereby customer acquisition costs doubled and conversion rates declined by 20 percent all of which were possible in a constraining digital advertising environment. With this, the timeline of the startup to break even in terms of EBITDA was delayed by close to two years and the planned runway based on the amount of funding sought could no longer be maintained. This led to restructuring of the fundraising round and a larger equity cushion was created. This was one of the most valuable exercises the founders of the startup have done later, as it helped them to think about the circumstances under which their model would not succeed.

A third example is a manufacturer which is backed by a private equity and which is about to refinance the debt. With the input commodity prices, revenue volume and interest rates all moving down at the same time, the advisors of the company developed a comprehensive stress test. The conclusion was that in an extreme yet realistic scenario, the interest coverage ratio of the company would drop to a level of less than 2.0x covenant as requested by the lenders. This understanding triggered the deal team to agree with a covenant holiday during the first year of the refinancing – something they would not have demanded without the stress testing analysis. In each of the three instances, the importance of stress testing did not lie in the future but in the mapping of the landscape of risk and making more informed decisions.

Common Challenges and How to Overcome Them

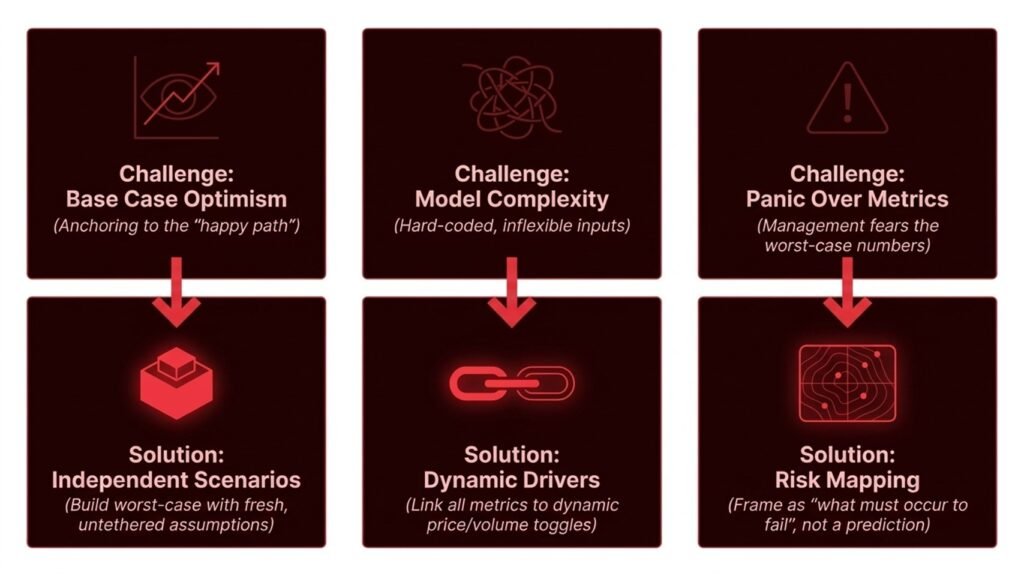

Among the most tenacious issues of stress testing is what practitioners term as the base case optimism bias. Analysts and especially those who are in close contact with the management teams can base their thought process on the base case and assume that it is a certainty. The negative and stress cases are nominal exercises – technically there in the model, but not really challenged. It is an acquired task to overcome this bias: the stress cases have to be constructed separately, with new assumptions, not as a percentage reduction off of the base case. One of the best ways to deal with this tendency is a scenario based financial modeling course that teaches scenario first thinking – establishing the world prior to filling in the numbers.

The second challenge is complexity of the model. Stress testing can be used to identify the weaknesses in model design. Unless your revenue assumptions are not hard-coded, but connected to volume and price drivers, then you cannot effectively stress those elements. Assuming that your working capital is a fixed ratio of revenue, as opposed to a ratio of payable and receivable days, the model would not be realistic at a stress test. The art of stress testing is also such a quality control, in other words: a model that cannot be well stressed has structural flaws that would bring down any analysis that relies on it.

The third difficulty is how to convey some form of uncertainty without compromising confidence. In a situation where a stress test shows that a firm has lost its liquidity buffer in an unfavorable condition, management may at times respond by doubting the scenario than looking into the risk in the business. The good analyst will not make predictions but draw stress test results in the form of risk maps – they will indicate what circumstances will have to happen in order to put the business at risk, and how probable or improbable those circumstances are. Such framing ensures that the discussion is more fruitful and that the analyst is seen as a risk advisor and not a pessimist.

Table 3: Scenario Building Process Flow for Fundraising Models

| Phase | Activity | Key Questions to Answer |

| Define | Pre-establish the boundaries and triggers of the scenario. | What are the circumstances of each situation? |

| Research | Collect past and market statistics. | What are the precedents to these assumptions? |

| Model | Develop connected assumptions into the model. | Do all drivers work dynamically and auditing? |

| Test | Check outputs and run each scenario. | Are there logical behaviour of outputs? |

| Communicate | Number to story. | What is the implication of this to the decision? |

Integrating Stress Testing into Valuation and Fundraising

Stress testing is not merely a risk management instrument, it is also becoming a competitive edge in raising funds and investor relations. Advanced investors, especially those to have attended a startup valuation and fundraising masterclass, will regularly execute their own stress tests as part of due diligence. Founders and CFOs who come with pre-assembled stress scenarios not only waste less time in the diligence process, but also indicate some kind of financial maturity that will instill investor confidence. A model that indicates that the business will be able to survive a reduction in revenue by 25 percent with 12 months left on the runway is much more convincing than one that merely indicates a positive growth trend.

Stress testing and the discount rate interact in a manner that is not well-understood in the context of valuation. A typical discounted cash flow analysis uses one weighted average cost of capital to a stream of cash flow anticipated to be used. However, the risk profile of those cash flows should be reflected in the appropriate discount rate, and stress testing can be used to measure the risk. When the cash flows of a business are very stable even when the business is in stressful situations i.e. when the business has long term contracted revenues then a low discount rate is warranted. When the cash flows fall in a worst-case scenario, even a simple, modest adverse scenario, then a higher risk premium is justified. This reasoning has to be incorporated into a valuation model, and it is an art that learners of rigorous financial modeling courses learn through time.

Institutional lenders and even individual credit funds are also increasingly demanding that borrowers should be able to come up with acceptable stress test analysis as a component of their financing applications. In leveraged acquisitions, such as, it has become a common practice to model the business at a 20 to 30 percent haircut of EBITDA and to show that the debt service level can be serviceable. Other lenders have also started to demand scenario analyses which incorporate commodity price stress, FX stress, and customer concentration stress – each considered individually, and then combined into a composite scenario. Mastering this level of stress testing is not an option, but a minimum requirement to work in credit and corporate finance at the intersection.

Table 4: Sample Scenario Assumptions — Technology Company (Illustrative)

| Assumption | Base Case | Downside Case | Stress Case |

| Revenue growth (Year 1) | 25% | 10% | -5% |

| Gross margin | 68% | 62% | 55% |

| Customer churn (monthly) | 2.0% | 3.5% | 6.0% |

| CAC (vs. base) | Base | +20% | +50% |

| Operating cost growth | 15% | 15% | 10% |

| Cash runway (months) | 24 | 16 | 9 |

Conclusion: Actionable Insights for Finance Professionals

The stress testing and sensitivity analysis are not high-level skills and are only executed by highly experienced professionals, however, they are basic skills that each finance specialist must acquire at the beginning of their career. It is good to hear they can be learned by means of systematic practice. In deepening your skills by taking courses in financial modeling, preparing to talk to investors as part of a startup valuation and fundraising masterclass, or, in a scenario based financial modeling course, creating more rigorous models, the concepts discussed in this article are directly relevant.

The initial practical lesson is to not add stress testing to any model post-hoc, but to make it a part of the model. Make your model in such a way that you can toggle scenarios, have visible and labeled assumptions and dynamically connected outputs to inputs. This architecture is a little bit more costly to construct but has dividends each time the model is applied to make a decision.

The second lesson is to base your assumptions of stress on evidence. Refer to historical data, industry reports and similar business cases. A stress situation based on what in fact occurred in previous recessions is much more convincing – and helpful – than one based on conjecture. The third lesson is to train to transform quantitative results into understandable stories. The bottom-line profit figure is often not the most important figure in a stress test, but instead a certain ratio: the interest coverage ratio, the debt-to-equity ratio or the months of cash runway. Be aware of the metrics that are important to your audience and start with them.

Lastly, do not think of any one of the stress tests as a compliance exercise but rather as a learning one. The true worth of doing a severe stress scenario is not to forecast disaster, but to see where the business will be the weakest and what measures can be taken in advance to make the business less vulnerable. Those analysts who share this attitude – who view models as living mechanisms to continue managing risks, and not as a product – are often some of the most useful members of any finance department. The abilities can be affordable; the practice can be to construct the habit.